Shopper walking past the Gucci store in Jiefangbei, Chongqing, China. Image credit: Shutterstock, Vincent Nguyen

Shopper walking past the Gucci store in Jiefangbei, Chongqing, China. Image credit: Shutterstock, Vincent Nguyen

Drawing on a survey of 3,000 aspirational luxury shoppers, new research reveals a Chinese luxury market in cautious recovery, where strong confidence coexists with disciplined budgets, growing “local love” for Chinese brands, and a reshaped channel mix in which official and travel-retail formats move to the center.

Key findings at a glance

- Per capita luxury spend is expected to decline by around 4 percent, even as most buyers feel positive about the economy and their own income

- Chinese luxury brands’ share of spend is set to rise from 39 percent to 44 percent, especially in jewelry

- Big-ticket categories take the hit, with planned spend on large leather goods down about 7 percent and on watches down 6 percent

- Travel retail becomes a core pillar alongside official boutiques and ecommerce, with mainland airports and Hainan among the top planned purchase locations

China’s luxury buyers are not walking away from the category, but they are quietly reshaping its balance of power.

Per a new report from management consultancy Kearney titled China luxury market: The ridge path toward a cautious recovery, shoppers plan to trim their average luxury budgets and cut back on large leather goods and watches, while redirecting more of their spend to Chinese brands and to trusted official and travel-retail channels.

“Chinese luxury buyers are not walking away, but they are making brands justify every purchase,” said Fabian Lux, partner at Kearney and co-author of the report.

The result is a market that still looks cautiously optimistic from the outside, but where global houses now face tougher, more locally attuned competition for every yuan, according to the report.

The report is based on a proprietary Kearney survey of 3,000 Chinese aspirational luxury shoppers conducted in August 2025. The sample covers Gen Z (18–28), millennials (29–44), and Gen X and boomers (45-plus) across first tier, “new” first tier and other cities.

Respondents mainly buy upper- and luxury-priced items in fashion and small accessories, large leather goods, watches, jewelry, and perfumery and beauty. They were asked about their sentiment, spending intentions and channel preferences for 2026.

Optimism stays high, but wallets tighten

Headline sentiment remains strikingly upbeat, per the report.

Around four in five respondents expect China’s overall economic situation to improve over the next 12 months, feel confident about their job and income stability, and trust the effect of policy support.

But that optimism comes with a limit.

On average, shoppers say they will slightly reduce their per capita luxury spend in the year ahead, with budgets expected to dip by about 4 percent compared with the past 12 months.

In other words, the core luxury buyer is still very much in the market, but with a more deliberate approach to where each yuan goes.

Chinese Year of the Horse 2026. Image credit: Shutterstock, Savanevich Viktar

Chinese Year of the Horse 2026. Image credit: Shutterstock, Savanevich Viktar

Big-ticket luxury takes the hit

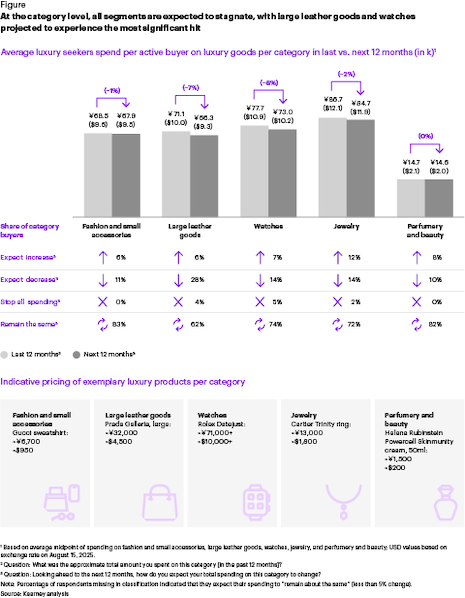

The outlook by category is one of stagnation rather than collapse.

Among active buyers, spending plans in “everyday luxury” segments are broadly flat: fashion and small accessories are expected to decline by about 1 percent and jewelry by around 2 percent, while perfumery and beauty remains roughly stable.

The real pressure falls on the iconic big-ticket purchases that once symbolized China’s luxury boom.

Planned spending on large leather goods is forecast to drop by about 7 percent, and watches by roughly 6 percent, making these categories the main contributors to the overall slowdown.

Beneath the surface, the report highlights a sharper divide between consumer groups.

Middle-aged, high-income shoppers in first-tier cities show the strongest drive for recovery and higher spending and continue to anchor premiumization.

Younger and lower-income cohorts, by contrast, are more cautious, with more respondents in these segments planning to reduce or pause purchases altogether.

Savings, experiences and tariffs reshape demand

For those intending to spend less on luxury, the issue is not so much a loss of appetite as a reprioritization of where money goes.

Among this group, close to half say their main motivation is to build up savings, while a significant share plans to redirect part of their budget from goods to experiences such as travel, events and culture.

That tilt toward experiences is particularly pronounced among younger consumers: the shift is strongest for Gen Z and millennials, where around 41 to 44 percent mention it, compared with about 31 percent for older generations.

This recalibration takes place against a backdrop of persistent macroeconomic and geopolitical uncertainty.

While the report does not attempt to forecast the wider economy, respondents point to factors such as employment prospects, consumer prices, real estate, interest rates, equity markets and global tensions as important in shaping how much they feel comfortable spending on luxury over the next 12 months.

Trade policy emerges as a sharp behavioral trigger.

Around three-quarters of surveyed shoppers say changes to U.S.–China tariffs will influence their purchasing decisions.

Roughly half are ready to shift at least part of their luxury spend to domestic Chinese brands, while close to six in 10 say they would avoid products made in the United States or favor U.S. brands manufactured elsewhere.

Snapshot of a market on a “ridge path”

To show how these forces interact, the Kearney report brings together the core shifts in a consolidated view of the market’s trajectory.

The study maps the “ridge path” of China’s luxury demand, bringing together how optimistic sentiment coexists with flatter budgets, bigger expectations of value, structural reallocation of spend across categories, brands and channels, and showing how the market is moving from easy expansion to a narrower, more demanding growth path.

All luxury segments are expected to stagnate at the category level, with large leather goods and watches expected to take the most significant. Source: Kearney

All luxury segments are expected to stagnate at the category level, with large leather goods and watches expected to take the most significant. Source: Kearney

“Local love” and travel retail move to the center

One of the clearest structural shifts in the study is the rising share of spend going to Chinese luxury labels.

Across categories, their share is expected to climb from 39 percent over the past 12 months to 44 percent in the year ahead.

Jewelry leads this “local love” trend, while perfumery and beauty stands out as the only category where international brands retain—or slightly increase—their relative position.

Channel strategies are also being rewritten.

The survey shows a hierarchy of planned purchase points in which “official” formats dominate and travel retail is firmly in the mainstream.

Official offline boutiques are cited by 56 percent of respondents, with official online channels close behind at 44 percent.

Mainland airports, also at 44 percent, and Hainan, at 39 percent, now sit alongside them as core purchase locations, well ahead of unofficial and grey-market channels.

Eventually, around six in 10 consumers indicate they will lean more heavily on duty-free channels as part of their response, reinforcing the shift in spend toward travel retail.

Overseas shopping remains part of the story, but the days of unchecked, daigou-fueled growth are over.

Around 36 percent of respondents plan to purchase luxury items outside mainland China in the next 12 months, and most of them expect those purchases to account for less than 30 percent of their overall luxury spend.

Millennials are the most outward-looking cohort: 43 percent intend to buy overseas, with these transactions representing around 28 percent of their luxury budget.

When Chinese consumers do buy abroad, they are not simply hunting for discounts.

The report finds that authenticity is the No. 1 reason to purchase luxury goods overseas, ahead of pricing, access to new releases or broader assortment.

Large leather goods and watches are particularly likely to be bought outside Asia, reflecting their high price point and the premium placed on trust.

Tougher, more demanding buyer raises the bar

If demand in China is disciplined rather than disappearing, the strategic challenge for luxury brands is how to turn that discipline into growth.

The study suggests that Chinese consumers are tightening expectations across almost every dimension of the brand relationship, rewarding only those players that can convincingly justify their price and position.

Respondents say they are more likely to increase spending with brands that feel genuinely desirable and relevant, but also demonstrably trustworthy and safe. They look for visible quality and longevity in materials and craftsmanship, distinctive in-store experiences backed by reliable after-sales service, and products and storytelling that are clearly tailored to Chinese tastes, culture and heritage.

Exclusive editions and memorable brand experiences still matter, but only when they come with clear value for money and consistent product availability, rather than as stand-alone theatrics.

IN THIS ENVIRONMENT, the margin for error narrows.

A misstep on value, authenticity or local relevance can quickly push spend toward rivals, especially increasingly capable local competitors.

“The winners in this challenging phase will be those that make trust unmistakable, localize with nuance and inspire desire without relying on price too much,” Kearney’s Mr. Lux said.

“For international brands, the right posture will mirror consumers’ behaviors: confident enough to invest and disciplined enough to adapt,” he said.